Demystifying Real Estate Financing: A Look at Fix-and-Flip, New Construction, Bridge, and DSCR Loans

Navigating the world of real estate financing can be daunting. Understanding the nuances of different loan programs is crucial for success, whether you’re a seasoned investor or just starting out. Let’s break down the key terms of four common loan types: Fix-and-Flip, New Construction, Stabilized Bridge, and DSCR.

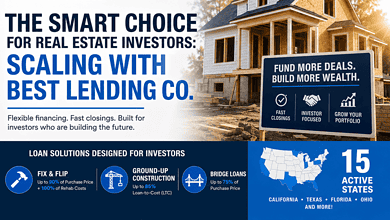

1. Fix-and-Flip Loans: Fast Funding for Quick Turnarounds

Fix-and-flip loans are designed for investors who purchase properties, renovate them, and resell them for a profit. Here’s what you need to know:

- Loan Amount: $50,000 to $5 million, accommodating a range of project sizes.

- Eligible Properties: Single-family residences (SFR), 2-4 unit properties, planned unit developments (PUDs), and warrantable condos.

- Loan-to-Value (LTV): Up to 70%, with 90% of the purchase price and 100% of the rehab costs covered.

- Loan Term: 12-18 months, aligning with the typical fix-and-flip timeline.

- Credit Score: Minimum 620 FICO score.

- First-Time Investors: May face slightly stricter LTV requirements (70-75%).

Key Takeaways:

- These loans prioritize speed and are designed for projects with a short turnaround time.

- The ability to finance 100% of rehab costs is a major advantage.

2. New Construction Loans: Funding Ground-Up Projects

New construction loans provide capital for building properties from the ground up:

- Loan Amount: $50,000 to $5 million.

- LTV: Up to 75% with approved plans and permits, or 60% without.

- Construction Financing: 100% of construction costs can be financed.

- Total Project Cost: Maximum 80% of the total project cost, with a potential 85% LTC exception.

- Loan-to-After-Repair-Value (ARV): 70%.

- Loan Term: 12-18 months.

- Experience Required: 1-3 similar ground-up deals or GC license with pulled permits or heavy rehab experience.

- Credit Score: Mid-score of 680.

Key Takeaways:

- This loan type requires significant experience in construction.

- Obtaining approvals and permits is crucial for maximizing LTV.

3. Stabilized Bridge Loans: Short-Term Financing for Transitions

Stabilized bridge loans offer short-term funding for properties that are undergoing a transition, such as renovations or repositioning:

- Loan Amount: $75,000 to $3 million.

- Loan Limits: $1.5 million maximum for SFR, $3 million maximum for 2-4 unit properties.

- Loan-to-Cost (LTC): 85% with 100% of rehab cost covered.

- Credit Score: 660 FICO score.

Key Takeaways:

- These loans are useful for quickly accessing capital while a property is being stabilized.

- High LTC ratios allow for significant leverage.

4. Debt Service Coverage Ratio (DSCR) Loans: Focusing on Cash Flow

DSCR loans are designed for investors who focus on a property’s cash flow:

- Loan Amount: $75,000 to $5 million.

- Financing Options: 80% of purchase price, 75% cash-out, 80% rate and term refinance.

- Loan Terms: 30-year, 5-year, 7-year, 10-year, interest-only (I/O) ARM.

- Prepayment Penalties: 5-4-3-2-1 or 3-2-1.

- Credit Score: 660 FICO score.

- Occupancy: 100% for cash-out and rate-term refinances.

Key Takeaways:

- These loans are ideal for long-term investments where cash flow is a priority.

- The variety of loan terms and prepayment options provide flexibility.

Understanding these loan terms is crucial for making informed decisions and securing the right financing for your real estate investments. Always consult with a qualified lender to discuss your specific needs and project requirements.