High-Yield Commercial and Multifamily Land Financing in Primary and Secondary Markets

Securing capital for land acquisitions, horizontal development, and commercial bridge projects remains one of the most dynamic—and challenging—sectors of real estate finance. With traditional banks tightening their belts on speculative development and raw land, private lenders are stepping in to fill the void, particularly in the nation’s top Metropolitan Statistical Areas (MSAs).

For brokers, developers, and investors, understanding the exact parameters of these specialized loan programs is critical to a smooth execution. Here is a deep dive into the current landscape of commercial and multifamily land financing for primary (MSA ranks 1-10) and secondary (MSA ranks 11-25) markets.

The Sweet Spot: Target Properties and Loan Purposes

Lenders operating in this high-yield space are prioritizing prime locations. The core focus remains firmly on Top 25 MSAs, where demand and liquidity provide a safety net for land and development plays.

Eligible property types include:

- Commercial Improved and Zoned Land

- Multifamily Improved and Zoned Land

- Single-Family Rental/Investment properties (Strictly non-owner-occupied/no homestead)

Supported Loan Purposes: Whether an investor is looking to break ground or reposition an asset, these programs are designed for transitional phases. Eligible purposes include acquisitions, refinancing, horizontal and vertical development, and bridge/rehab projects.

High-Yield Commercial &

Multifamily Land Financing

An executive breakdown of current lending parameters, leverage constraints, and risk factors for land acquisitions and bridge development in top MSAs.

Core Program Metrics

Baseline financial requirements and expected terms for tier 1 and tier 2 market land loans.

Maximum Leverage Constraints

Security is strictly limited to 1st Lien Positions. Lenders cap leverage aggressively on raw land compared to improved properties or total project costs.

Eligible Loan Purposes

Capital is deployed for transitional phases. Single-Family is restricted strictly to non-owner-occupied rental/investment properties.

The “Watch List”

These factors are not strictly prohibited but require substantial compensating factors such as low LTV or pristine credit.

Market & Location

- ⚠️ Tertiary Markets (MSA Rank 26+)

- ⚠️ Rural land lacking zoning/entitlements

- ⚠️ Single-Family land where inventory exceeds demand

Asset Classes

- 🛑 Hospitality

- 🛑 Heavy Industrial

- 🛑 Office & Retail

- 🛑 Environmental Issues / Flood Zones

Borrower & Deal Specs

- 📉 Lack of Borrower Experience

- 📉 Prior Bankruptcies / Foreclosures

- 📉 Unlikely Payoff Scenario

- 📉 Cost Exceeds Project Value

Execution & Closing Pipeline

A streamlined process is critical for land acquisition. Standard execution targets a 30-day window, heavily dependent on borrower responsiveness and deal complexity.

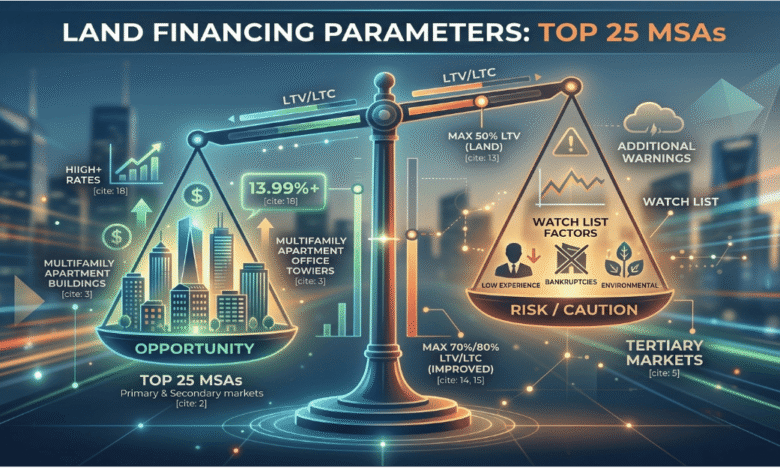

By the Numbers: Leverage, Pricing, and Terms

In exchange for the inherent risks of land and development financing, lenders are structuring these deals as short-term, high-yield bridge vehicles. Security is strictly limited to a 1st lien position (no second liens permitted).

Here is how the general loan parameters break down:

- Minimum In-Place Value: $1,000,000

- Loan Amounts: $500,000 minimum (Maximum amounts are typically TBD based on the specific deal profile).

- Maximum Leverage:

- Land: Up to 50% LTV (Subject to deal review)

- Improved/GUC: Up to 70% LTV

- Maximum LTC: Up to 80%

- Term & Extensions: Standard terms range from 12 to 24 months. Borrowers can typically secure a 6-month extension for a 1.0% to 2.0% fee.

- Rates & Fees: Interest rates currently start at 13.99% (interest-only). Origination fees sit at 3.0% of the total loan amount.

- Prepayment & Exit: While there is zero exit fee and technically no prepayment penalty, lenders require a guaranteed minimum of 6 months of interest based on the total loan amount.

- Reserves: Borrowers must maintain at least three months of payment reserves in an escrow account.

The “Watch List”: Proceed with Caution

Not all deals are created equal. While not explicitly prohibited, certain property types, locations, and borrower profiles are placed on a “Watch List.” To secure funding for these scenarios, sponsors must bring substantial compensating factors to the table, such as exceptionally low LTVs, pristine credit, or overwhelmingly positive market conditions.

Market & Asset Watch List:

- Tertiary Markets (MSA Rank 26+) and rural land lacking zoning or entitlements.

- Higher-risk commercial sectors including hospitality, heavy industrial, office, and retail.

- Single-family zoned land or horizontal development in markets where inventory currently exceeds demand.

Borrower & Deal Watch List:

- Lack of borrower experience or prior bankruptcies/foreclosures.

- Deals where the cost exceeds the project value or the ultimate payoff seems unlikely.

- Assets facing environmental issues or located in flood zones.

Execution and Closing

Speed is the ultimate currency in private land and development financing. Deals in this program generally target a ~30-day timeline to close, starting from the execution of the term sheet and receipt of the diligence deposit. (Naturally, timeframes can expand based on deal complexity, size, and borrower responsiveness).

To kick off the process, borrowers should expect to post a diligence deposit—minimums are typically set at $20,000 for non-construction loans and $40,000 for construction loans, subject to the deal’s specific requirements.

The Bottom Line

For developers and investors operating in the nation’s top 25 MSAs, robust capital is available for commercial and multifamily land projects. By understanding these leverage constraints, pricing models, and “watch list” triggers, originators can confidently match their sponsors with the right capital to get their projects out of the ground.