Invoice Factoring vs. Accounts Receivable Financing: A Complete Guide for B2B Companies

If your business invoices other businesses and waits 30, 60, or 90 days to get paid, you’re essentially providing your customers with an interest-free loan — funded by your own cash flow. Invoice factoring and accounts receivable (A/R) financing are two distinct mechanisms that let you stop waiting and start operating on your customers’ invoice balances today.

They’re often used interchangeably, but they’re structurally different products with different costs, relationships, and balance sheet implications. This guide breaks down both — clearly.

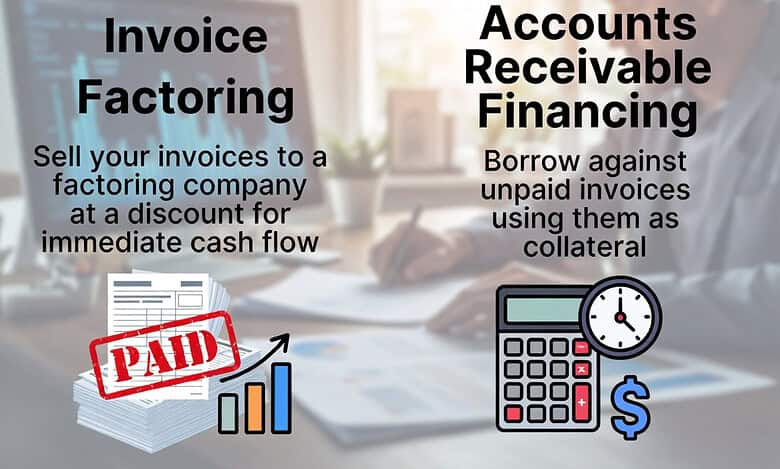

The Core Difference: Sale vs. Collateral

| Feature | Invoice Factoring | A/R Line of Credit (Financing) |

| Structure | You SELL your invoices to the factor | You use invoices as COLLATERAL for a loan |

| Balance Sheet | Removes A/R from your balance sheet | A/R remains; liability is added |

| Customer Notification | Yes — factor collects directly from customer | Usually no — you collect, then pay lender |

| Advance Rate | 80% – 95% of invoice face value | 75% – 90% of eligible A/R |

| Cost | 1.5% – 5% of invoice (flat fee or weekly rate) | Prime + 2% – 6% annually |

| Best For | Small/growing businesses, weak credit | Established businesses with strong bank relationships |

How Invoice Factoring Works

When you factor an invoice, you are selling a receivable. Here’s the step-by-step process:

- Step 1 — Issue Invoice: Your business delivers goods or services and invoices your customer (the ‘account debtor’) for, say, $100,000 with net-60 terms.

- Step 2 — Submit to Factor: You submit the invoice to the factoring company. They verify it’s a legitimate, undisputed invoice from a creditworthy customer.

- Step 3 — Receive Advance: The factor advances you 80%–95% of the invoice value — $80,000 to $95,000 — within 24–48 hours.

- Step 4 — Customer Pays Factor: On Day 60, your customer pays the factor directly (they are notified of the assignment).

- Step 5 — Receive Rebate: The factor remits the remaining balance (the ‘reserve’) minus their fee. If the fee is 3% ($3,000), you receive the remaining $17,000 ($20,000 reserve minus $3,000 fee).

Your total cost: $3,000 on a $100,000 invoice to receive $80,000 in 24 hours instead of waiting 60 days. Whether that’s expensive or cheap depends entirely on what you can do with that $80,000 for 60 days.

Recourse vs. Non-Recourse Factoring

This is the most important structural distinction within factoring:

- Recourse factoring: If your customer doesn’t pay the invoice, you must buy it back from the factor. You bear the credit risk. Lower fees.

- Non-recourse factoring: If your customer goes bankrupt or simply doesn’t pay (for credit reasons), the factor absorbs the loss. You do not have to repay the advance. Higher fees — but you’re essentially buying bad debt protection.

Most factoring is recourse factoring for straightforward non-payment disputes. Non-recourse protection typically only applies to customer insolvency, not invoice disputes.

How Accounts Receivable Financing (A/R Line) Works

An A/R revolving line of credit works more like a traditional bank product. Your accounts receivable serve as collateral, but you retain ownership of them and continue to manage the collection relationship with your customers.

- The lender establishes a borrowing base — typically 75%–90% of eligible A/R (invoices that are undisputed, less than 90 days old, and not concentrated beyond a single customer limit)

- You can borrow against the borrowing base at any time, up to a pre-approved line limit

- As customers pay invoices, the paid A/R is removed from the borrowing base and you must pay down the corresponding amount on the line

- Interest accrues daily on your outstanding balance — not on your total A/R

Because the lender does not collect directly from your customers, this structure maintains your customer relationships. The lender typically files a UCC-1 lien on your A/R as part of the security agreement.

Who Uses Invoice Factoring?

Factoring is particularly common — and well-suited for — industries with long payment cycles and creditworthy institutional customers:

- Trucking and freight (pay-when-paid cycles from brokers and shippers)

- Staffing agencies (slow-paying Fortune 500 clients)

- Government contractors (federal agencies can take 45–90 days to pay)

- Construction subcontractors (pay-when-paid general contractor relationships)

- Wholesale and manufacturing (net-60 and net-90 terms are standard)

Calculating the True Cost of Factoring

Factoring fees are quoted in various ways that make apples-to-apples comparison difficult. Always convert them to an annualized rate (APR) to make a rational comparison against other forms of financing.

Example: A factor charges a 1% weekly fee on outstanding invoices. An invoice that takes 4 weeks to pay has a fee of 4%. Annualized: 52 weeks × 1% = 52% APR equivalent.

That sounds shocking — until you compare it to the cost of turning down a large order because you don’t have the working capital to fulfill it. The relevant comparison isn’t the APR. It’s the ROI on the capital deployed.

Which Is Right for Your Business?

Choose invoice factoring if you’re a smaller or younger business that needs immediate cash, has limited banking relationships, or serves a concentrated set of creditworthy enterprise customers. The higher cost and customer notification trade-off are acceptable to get capital now.

Choose an A/R line of credit if you’re an established business with a banking relationship, a diversified customer base, and the operational capacity to manage collections yourself. The lower cost and invisible financing make the A/R line a more strategic, scalable solution.

Lender Tribune connects B2B businesses with both factoring companies and asset-based lenders. Tell us your revenue, industry, and average invoice size, and we’ll match you with the right product.