SBA 7(a) vs. SBA 504 Loans: Which Is Right for You?

SBA loans are government-backed commercial financing products designed to provide small businesses with access to capital that may be unavailable through traditional conventional lending. While the Small Business Administration (SBA) does not lend money directly, it provides a federal guarantee to your lender, reducing their risk and allowing for lower down payments and longer repayment terms.

At Lender Tribune, we help you navigate the two most popular federal programs: the 7(a) and the 504. Choosing between them depends entirely on what you intend to do with the funds.

7(a) vs. 504: The Core Differences

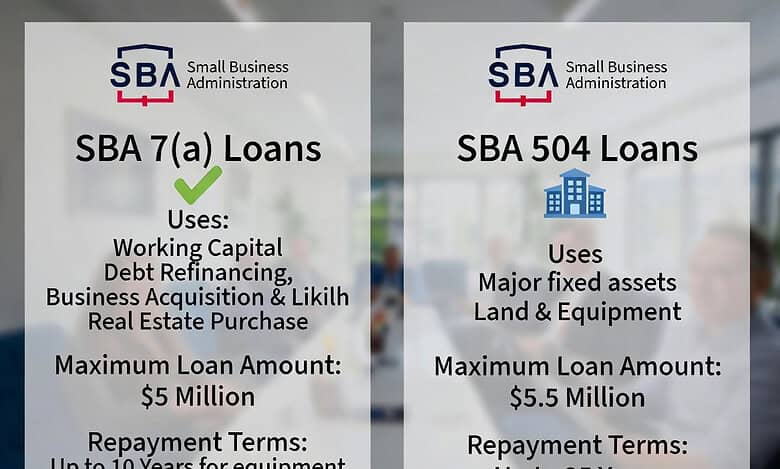

The 7(a) is the SBA’s “all-purpose” tool, while the 504 is a specialized “economic development” tool designed for major fixed assets.

| Feature | SBA 7(a) Loan | SBA 504 Loan |

| Best Used For | Working capital, inventory, business buyouts. | Real estate and heavy machinery. |

| Maximum Amount | $5 million | Over $5.5 million (Project-based) |

| Down Payment | 10% to 20% | 10% (Strict) |

| Interest Rates | Variable or Fixed (Prime + Spread) | Fixed (Below-market institutional rates) |

| Repayment Term | 10 years (Business) / 25 years (RE) | 10, 20, or 25 years |

| Structure | Single lender (Bank) | Bank + CDC + Borrower |

Deep Dive: The SBA 7(a) Loan

The 7(a) is the most flexible loan in the SBA’s arsenal. If you are looking to acquire an existing business or need a large infusion of working capital to scale, this is your primary vehicle.

Key Advantage: Flexibility

Unlike the 504, the 7(a) can be used for “soft” costs and intangible assets. This makes it the go-to choice for:

- Goodwill/Business Acquisitions: Buying the reputation and client list of a competitor.

- Debt Refinancing: Rolling high-interest credit cards or short-term debt into one 10-year loan.

- Working Capital: Funding payroll, marketing, and inventory.

The Downside: Variable Rates

Most 7(a) loans are pegged to the WSJ Prime Rate. Because they are variable, your monthly payment can increase if the Federal Reserve raises interest rates.

Deep Dive: The SBA 504 Loan

The 504 program is structured specifically for owner-occupied commercial real estate and long-term equipment. It is designed to create jobs and promote community growth.

The 50-40-10 Structure

The 504 loan is unique because it involves three parties. This structure is what allows for the ultra-low 10% down payment:

- The Bank (50%): A traditional lender provides a first mortgage for 50% of the project.

- The CDC (40%): A Certified Development Company (SBA-backed nonprofit) provides a second mortgage for 40%.

- The Borrower (10%): You provide a 10% down payment.

Key Advantage: Fixed, Long-Term Rates

The 40% portion provided by the CDC is a fixed-rate, fully amortizing loan. This protects your business from market volatility for 20 to 25 years.

Calculating Your SBA Loan Payment

Note: Use this plain-text math for easy WordPress pasting.

Both SBA loans are fully amortizing, meaning your monthly payment includes both principal and interest. To calculate your estimated monthly payment (M), use this formula:

M = P × [ r(1 + r)^n / ( (1 + r)^n – 1 ) ]

- P = Loan amount

- r = Monthly interest rate (Annual rate / 12)

- n = Number of months (120 for 10 years; 300 for 25 years)