Merchant Cash Advances (MCAs): Risks, True Costs, and When Alternatives Are Smarter

Merchant cash advances are the most misunderstood — and most misused — financial product in the small business lending market. They’re not loans. They’re not regulated like loans. And their effective cost, properly calculated, would horrify most business owners who sign MCA agreements without fully understanding the math.

That’s not an argument to never use an MCA. There are legitimate use cases. But every business owner who touches MCA capital needs to understand exactly what they’re getting into before signing a contract.

What Is a Merchant Cash Advance?

An MCA is a purchase of future receivables. The MCA provider gives you a lump sum of capital today in exchange for a fixed dollar amount of your future revenue — collected as a daily or weekly percentage of your credit card sales or total bank deposits (ACH).

Key terms to understand:

- Advance Amount: The cash you receive. Example: $100,000.

- Payback Amount (Factor Rate × Advance): What you pay back. A 1.40 factor rate means you pay back $140,000 on a $100,000 advance.

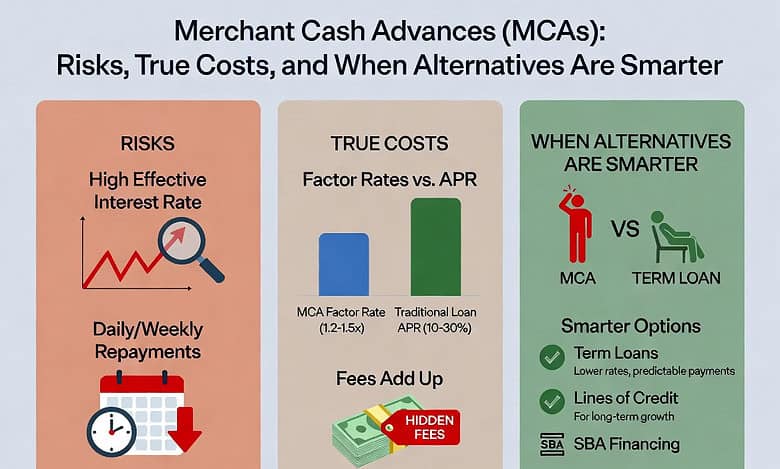

- Factor Rate: Expressed as a decimal (1.15 to 1.55+). This is NOT an interest rate. It does not decrease as you pay down the balance.

- Holdback Percentage: The daily or weekly percentage of sales deducted. Example: 15% holdback on $2,000/day in credit card sales = $300/day in deductions.

- Estimated Term: Not a fixed term. Duration depends on your sales volume. Higher revenue = faster payoff.

The True Cost of an MCA: An Honest Calculation

MCA providers quote factor rates, not APRs, because the APR would deter most borrowers. Here’s how to calculate the actual annualized cost:

| Variable | Example Value | Notes |

| Advance Amount | $100,000 | Cash received |

| Factor Rate | 1.40 | Common for first-time MCA borrowers |

| Total Payback | $140,000 | 100,000 × 1.40 |

| Total Cost (Dollar) | $40,000 | The fixed fee — never changes |

| Estimated Payback Period | 6 months | Based on holdback % and revenue |

| Annualized APR Equivalent | ~80% | (40,000 / 100,000) × (12/6) = 80% |

At a 1.40 factor rate paid back over 6 months, your effective APR is approximately 80%. If you pay it back faster (because your sales are strong), the APR is even higher — because you’re paying the same $40,000 cost in less time. This is the inverse of how traditional loan interest works and why MCAs are so expensive for fast-growing businesses.

The MCA Debt Trap: How Businesses Get Stuck

The most dangerous MCA scenario is called ‘stacking’ — taking a second or third MCA before the first is paid off. Here’s how the trap typically develops:

- Business takes a $50,000 MCA at 1.35 factor rate. Daily deduction is $900.

- Daily deduction strains cash flow. Revenue dips. Owner can’t make payroll.

- Owner takes a second MCA for $40,000 to cover the cash shortfall. Now daily deductions total $1,600.

- Both MCAs are now competing with payroll and vendor payments. Business falls behind on rent.

- Owner takes a third MCA. The daily deduction is now $2,400. The business is in a death spiral.

MCA providers are aware of this dynamic and many actively solicit renewal offers before the prior advance is paid off. Decline these offers unless you have an extremely clear, time-limited need for capital.

When an MCA Actually Makes Sense

Despite the costs, MCAs have legitimate use cases in specific, time-limited scenarios:

- Seasonal inventory purchase: A retailer needs $80,000 to stock for the holiday season. The inventory will sell in 60 days at a 40% margin. The MCA cost ($8,000–$12,000) is a small fraction of the generated profit.

- Emergency equipment replacement: A restaurant’s walk-in freezer fails on a Friday. A 48-hour MCA gets the replacement funded. The alternative — losing inventory and closing for a week — costs more than the MCA fee.

- Bridge to approved SBA or bank loan: A business has a term sheet for a conventional loan that closes in 45 days but needs cash now. The MCA bridges the gap for a defined, short period.

What MCAs are not for: ongoing working capital deficits, payroll, or cash flow problems that indicate a structurally unprofitable business. Using expensive capital to mask an underlying business problem delays the inevitable and makes the eventual reckoning more severe.

MCA Alternatives to Consider First

Before signing an MCA agreement, exhaust these options:

- Business Line of Credit: If you have 2+ years in business and $250K+ in revenue, you likely qualify for a revolving line of credit at 15%–30% APR — a fraction of MCA cost.

- Invoice Factoring: If your cash flow problem stems from slow-paying customers, sell those invoices rather than your future revenue. Lower cost for B2B businesses.

- SBA 7(a) Working Capital Loan: Longer processing time, but 10%–12% APR vs. 60%–150% APR equivalent on an MCA.

- Equipment Financing: If the capital need is asset-specific (equipment, vehicle), equipment financing at 8%–15% APR is far cheaper than MCA.

- Revenue-Based Financing: Some specialty lenders offer revenue-based financing (RBF) with factor rates of 1.10–1.25 and monthly (not daily) repayment. A meaningfully better product.

MCA Contract Red Flags: What to Review Before Signing

MCA agreements are not regulated by federal lending laws (because they’re not classified as loans) and can contain provisions that would be prohibited in a traditional loan contract. Before signing:

- Confirm the total payback amount — verify: advance × factor rate = total obligation

- Understand the holdback percentage and estimate your daily payment based on your actual deposit volume

- Check for a ‘confession of judgment’ clause — some MCAs include COJ provisions that allow the lender to obtain a court judgment against you without notice in certain states. This is predatory and should be a deal-breaker.

- Verify there is no prepayment discount — MCAs are priced on total payback, not time. Paying early rarely saves you money unless the contract specifies a discount.

- Understand the default provisions — what happens if your daily deposits drop below a threshold

If you’re considering an MCA, Lender Tribune recommends first submitting your scenario to our network to see if a better product is available. We work with lenders across the credit spectrum and can often find term loan, line of credit, or revenue-based alternatives with meaningfully lower total cost.