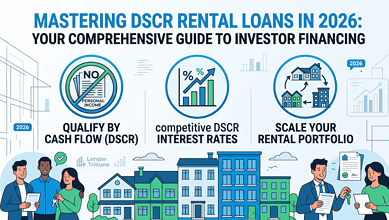

As we move deeper into 2026, the DSCR (Debt Service Coverage Ratio) loan has become one of the most powerful tools in a real estate investor’s financing arsenal. Unlike traditional mortgages that rely heavily on personal income documentation, DSCR loans evaluate the property itself — its rental income potential — to determine qualification. This makes them ideal for investors who want to scale their portfolios without jumping through hoops on tax returns and employment verification.

In this comprehensive guide, we will cover everything you need to know about DSCR loans in 2026, including current requirements, interest rates, and how to position yourself for approval.

What is a DSCR Loan?

A DSCR loan is a financing option that uses the property’s cash flow to determine eligibility. The debt service coverage ratio measures the property’s net operating income (NOI) against its debt obligations. Simply put: Does the rent cover the mortgage?

The DSCR Formula:

DSCR = Net Operating Income / Monthly Debt Service

A DSCR of 1.0 means the property generates exactly enough income to cover the mortgage. Most lenders prefer a DSCR of 1.0 to 1.25, meaning the property has some buffer for unexpected expenses or vacancies.

2026 DSCR Loan Requirements

Minimum Credit Score

DSCR loans in 2026 typically require a minimum credit score of 620, though some lenders may accept scores as low as 550 with additional collateral or higher down payments. For the best rates, a score of 680+ is recommended.

Minimum DSCR

Most lenders require a minimum DSCR of 1.0 to 1.25. Some programs allow DSCR as low as 0.75, but this usually comes with higher interest rates and more stringent down payment requirements.

Down Payment Requirements

For DSCR investment property loans, expect to put down 20-25% of the purchase price. If you are doing a cash-out refinance, lenders typically want at least 25% equity in the property.

No Income Verification

One of the biggest advantages of DSCR loans is that they typically do not require verification of personal income. There are no tax returns, W-2s, or pay stubs needed. The property’s rental income is the key qualification factor.

Current DSCR Loan Interest Rates (2026)

DSCR loan rates in 2026 are competitive with traditional investment property loans:

- Excellent Credit (720+): 6.00% – 7.00%

- Good Credit (680-719): 6.75% – 7.75%

- Fair Credit (620-679): 7.25% – 8.50%

- Lower Credit (550-619): 8.50% – 12.00%

Rates vary based on the lender, property location, and loan terms. Adjustable-rate DSCR loans may offer lower initial rates, while fixed-rate options provide payment stability.

How to Calculate Your DSCR

Before applying, calculate your property’s DSCR to understand where you stand:

- Calculate Gross Rental Income: Monthly rent x 12 months

- Subtract Operating Expenses: Property taxes, insurance, maintenance, vacancy reserve (typically 5-10%), property management fees (if applicable)

- Determine NOI: Gross income – Operating expenses

- Calculate Debt Service: Monthly mortgage payment x 12

- Apply the Formula: NOI / Debt Service = DSCR

Example:

Property rents for $2,500/month ($30,000/year)

Operating expenses: $10,000/year

NOI: $20,000/year

Mortgage payment: $1,500/month ($18,000/year)

DSCR: $20,000 / $18,000 = 1.11

Types of DSCR Loans in 2026

1. Long-Term Rental DSCR

These are 30-year fixed-rate loans designed for properties you plan to hold long-term. They offer predictable payments and are ideal for building passive income.

2. Short-Term Rental DSCR

Also known as bridge DSCR loans, these are ideal for investors planning to renovate and sell (fix-and-flips) or properties with higher vacancy risk. Terms typically range from 1-5 years.

3. Cash-Out Refinance

Pull equity out of your existing rental properties to fund additional investments. Cash-out DSCR loans typically require at least 6 months of rental history and a DSCR of 1.0+.

4. Multi-Family DSCR

For 2-4 unit properties, multi-family DSCR loans work similarly to single-family programs but may have slightly higher rates due to increased complexity.

How to Improve Your Chances of Approval

- Maintain Strong Credit: Scores above 680 will qualify for the best rates.

- Choose Properties with Strong Cash Flow: Properties with DSCR above 1.25 are most likely to approve.

- Document Rental Income: Even though income verification is not required, having lease agreements and rent rolls strengthens your application.

- Reduce Other Debts: Lowering your personal debt-to-income ratio improves your overall financial profile.

- Work with an Experienced Lender: DSCR lending is specialized. Find a lender who understands investment properties and can guide you to the right program.

DSCR vs. Traditional Investment Loans

| Feature | DSCR Loan | Traditional Investment Loan |

|---|---|---|

| Income Verification | Not Required | Required (Tax Returns, W-2s) |

| Credit Score Minimum | 550-620 | 620-680 |

| Down Payment | 20-25% | 15-25% |

| Qualification Focus | Property Cash Flow | Personal Income + Credit |

| Loan Term | Up to 30 Years | Up to 30 Years |

Top DSCR Lenders for 2026

- Rivara Capital: Known for zero-reserve DSCR programs

- Sphinx Capital: Expanded access programs for Q1 2026

- Asset Based Capital Inc.: Modern approach to commercial lending

- Stallion Funding: Competitive rates and fast closing

Final Thoughts

DSCR loans are revolutionizing real estate investing in 2026 by making capital more accessible to investors regardless of their personal income situation. Whether you are a seasoned investor looking to scale or just starting with your first rental property, DSCR loans offer a pathway to building wealth through real estate without the traditional lending barriers.

Before applying, calculate your property’s DSCR, gather your rental documentation, and compare offers from multiple DSCR-specialized lenders. With the right approach, you can secure financing that helps your properties generate positive cash flow from day one.

For more information about DSCR loans and other real estate financing options, visit Lender Tribune.